Back in the day, we did a two-part series on Universal Life (UL) insurance policies, pointing out some of the pitfalls inherent in those plans. Since then, there've been some terrific advances, industry-wide, addressing these shortcomings. Called Guaranteed Death Benefit UL, they promised to keep the policy in-force regardless of whether or not there was sufficient (or any) cash value.

In a sense, these are term-to-age-100 (or even 120!) policies, since they're heavy on death benefit guarantees and pretty light on cash values. But for long term planning, they're difficult to beat.

So of course the National Association of Insurance Commissioners felt the need to step in and meddle:

"The [NAIC] adopted revisions to a controversially applied actuarial guideline that governs reserves for universal life products with secondary guarantees after almost a year of intense debate among regulators on all levels and the industry."

So what, you ask?

Here's what:

"For example, for certain policies, companies must “perform a good faith high-level analytical review of the product design with respect to the premium payment patterns to be expected with respect to that design.”

In short, look for premiums on newly written plans to be substantially higher than existing ones. And don't even think about messing around with your in-force policy (if you have one).

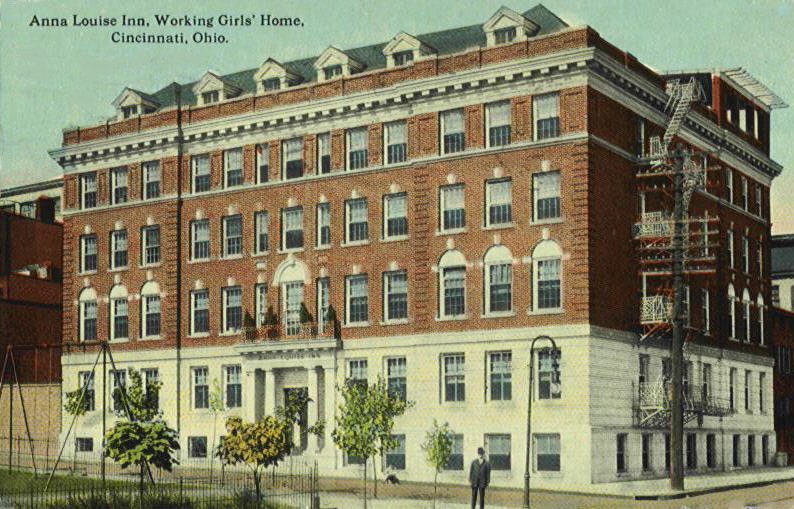

Maybe, maybe not. That question mark's there because it's not entirely clear that Fortune 500 company Western & Southern Life is really in the wrong here:

"Western & Southern .... has been trying for several years to buy or force the Anna Louise out of the Lytle Park Historic District, the beautiful and serene neighborhood they share, and turn it into a boutique hotel."

The current owner is Cincinnati Union Bethel, a non-profit that runs the facility, which "provides safe and affordable housing for women so they can live independently and within their means."

On the other hand, the folks at Western & Southern aren't necessarily bad guys just because they disagree with the Bethel folks:

"Our proposal for Anna Louise Inn, its owner Cincinnati Union Bethel and Lytle Park is a win-win for every stakeholder involved. It will cost taxpayers less; provide a new, improved facility for the residents of the Anna Louise; create economic opportunity for the city; and preserve the building and its historical significance."

In fact, there may be no "good" or "bad" guy here: sometimes organizations (and the people who support them) can have fundamental disagreements. From this vantage point, at least, I think both sides present compelling arguments; which one ultimately prevails is a matter for the courts.

One of the so-called "free" benefits of Obamacare is the ability to continue "children" under your group health insurance plan.

Free?

Really?As any actuary could have explained to Democrats had they taken the time toask, this mandate will dramatically drive up the cost of health insurance forchildren. Of course, they didn’t ask. They believed that by expanding healthcoverage to millions of uninsured people health spending, and thereforepremiums, would actually go down.

Most workers with employer-based coverage won’t see much of an increasebecause the employer providing their health insurance often covers most ofthe premium cost. Except, it turns out, for the military.

As the Wall Street Journal reports, “Families covered by Tricare, the healthprogram for active and retired members of the military, must pay as much as$200 a month to let an adult stay on their plan until age 26.”

That would be $2,400 for the first year of coverage for a family on a militarysalary. As President Obama might say, it’s arithmetic. If it’s two young adults,it’s $4,800 a year. Thank you for your service!

Forbes, "Military families get $2400 Obamacare bill"

{kind=link}